Until five weeks ago, the 1973 Arab oil embargo was the benchmark for energy disruption. 4.5 million barrels a day were removed from supply, crude prices quadrupled, and a decade of stagflation across the industrialised world ensued. That benchmark is now shattered. Since Iran shut the Strait of Hormuz on March 4, some 20 million barrels a day have been locked out of global markets, in what the head of the International Energy Agency has called the “greatest global energy security challenge in history”.

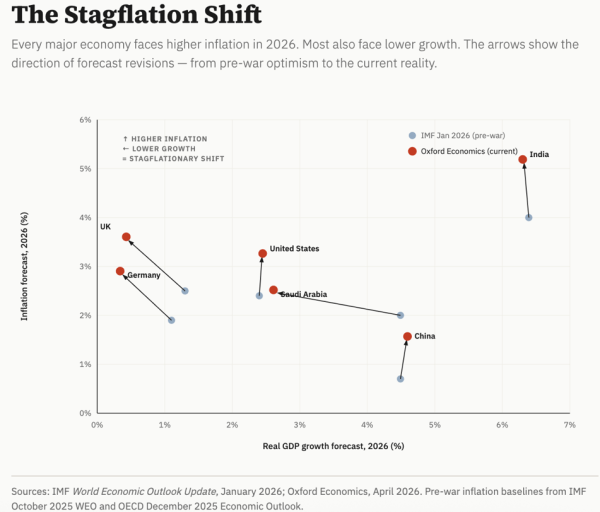

US gasoline has hit $4.11 a gallon, up 38 per cent, while diesel has surged 49 per cent to $5.62. Asian LNG spot prices have almost doubled after Iranian strikes crippled Qatar’s Ras Laffan complex. Oxford Economics, modelling a prolonged war scenario in which oil stays above $150 a barrel for four months, projects global inflation rising to 7.7 per cent. World GDP growth could slow down to just 1.4 per cent in 2026, 1.2 percentage points below baseline, with recessions in the US and most major advanced economies. That would represent, excluding the pandemic and the global financial crisis, the most severe coordinated slump in four decades.

But the 1973 parallel, frequently invoked, obscures a crucial distinction. In 1973, the shock was imposed on the United States by Arab producers retaliating against American foreign policy. In 2026, the shock originates in the United States, from a war of choice launched by the Trump administration without congressional authorisation and over allied objections, further compounding a simultaneous shock that also originated at the White House. The war alone would constitute a serious shock. But it lands on an economy already weakened by the most aggressive tariff regime in 80 years.

By late 2025, the administration had raised average US duties from 2.4 per cent to a post-war high of 9.6 per cent. Estimates showed an average household burden of $1,500 in 2026, the largest tax increase as a share of GDP since 1993. The OECD projects US growth nearly halving from 2.8 per cent to 1.6 per cent, with global growth dipping below 3 per cent for the first time since the pandemic. When the Supreme Court struck down the bulk of Trump’s emergency tariffs in February, the administration pivoted within a day to new levies under different statutory authority, with pharmaceutical tariffs flagged at up to 200 per cent. While the policy instrument has changed, the impulse remains the same.

Tariffs raise the cost of goods at the border, while the Hormuz closure raises the cost of moving everything everywhere. The Federal Reserve, which would ordinarily cut rates to cushion a growth slowdown, cannot do so with inflation threatening 3 per cent or higher. This is the stagflation trap of the 1970s reassembled, except that both jaws are being set by the same hand. In addition, the non-linearities are severe – supply-chain cascades and financial-market contagion amplify the pure energy-supply hit from 0.9 percentage points of lost GDP to a total deviation of 2.1 percentage points from baseline. If the shock triggers a sustained retreat in AI investment, or de-anchors inflation expectations, the damage could prove structurally permanent, raising long-term borrowing costs and altering how monetary policy responds to future shocks for years to come.

Figure 1

Source: Created with Claude using data collected by the author

India offers the starkest illustration of the compounding crisis at work. Last August, Trump imposed 50 per cent tariffs on Indian goods, among the highest levied on any partner, battering Indian equities into the worst-performing emerging market of 2025. In February, the rate was cut to 18 per cent, but only after New Delhi agreed to halt Russian crude purchases and pivot to Gulf and American supply. Weeks later, Trump’s war shut the very strait through which half of India’s crude and 90 per cent of its LPG imports flow. The rupee hit record lows, and the Reserve Bank of India burned through billions in reserves while the government slashed excise duties at enormous fiscal cost. A nation of 1.4 billion was whipsawed between Trump’s trade ultimatums and Trump’s military adventurism — two policies that actively contradicted each other.

The caveat is that other risks to the global economy exist. China’s property overhang persists. Sovereign debt burdens across the Global South remain elevated. The claim that one man constitutes the single greatest threat is, at the margin, an overstatement. No other actor on the world stage is simultaneously the architect of a trade war touching every major economy and a military war that has produced the largest oil supply disruption in recorded history. No other leader’s domestic policy and foreign policy are so visibly at cross-purposes, generating compounding costs that neither shock would produce alone. As IMF Managing Director Kristalina Georgieva observed, “All roads now lead to higher prices and slower growth.”

Bardhan is a Junior Fellow at the Observer Research Foundation